Canada’s economy, the second largest in North America with a nominal GDP of approximately 2.1 trillion dollars, combines structural strengths with persistent vulnerabilities. The country benefits from a stable banking system, abundant natural resources including oil, natural gas, minerals, and timber, a skilled workforce, and a diversified economic base spanning technology, manufacturing, agriculture, and services.

However, key challenges remain. Productivity growth continues to lag behind peer economies, housing affordability remains a critical concern, and household debt levels stay elevated. In addition, demographic pressures linked to an ageing population continue to weigh on long-term growth prospects.

Trade plays a central role in economic performance. The United States accounts for roughly 75% of exports and 52% of imports, followed by China, Mexico, and the European Union. Canada primarily exports crude oil, natural gas, refined petroleum, minerals, agricultural goods, and forest products, while imports consist largely of machinery, vehicles, chemicals, and consumer goods. A persistent trade deficit, averaging between 10 and 15 billion dollars annually in recent years, reflects strong domestic demand for imports and relatively weak manufacturing competitiveness.

Economic growth has remained subdued, expanding between 0.5% and 1.5% annually from 2022 to 2025, below the pre-pandemic average of 1.8%. This slowdown has been driven primarily by elevated interest rates and cautious consumer spending.

Inflation has moderated significantly since peaking at 8.1% in 2022, which prompted the Bank of Canada to raise interest rates aggressively from 0.25% to 5%. During 2024, the central bank began easing policy, cutting rates to approximately 3.75% by early 2025 as inflation cooled.

More recently, inflation has shown signs of reaccelerating, rising to 2.8% in April, the highest level since May 2024. Despite this increase, the figure came in below market expectations of 3.1%, suggesting weaker-than-anticipated price pressures.

Technical Analysis

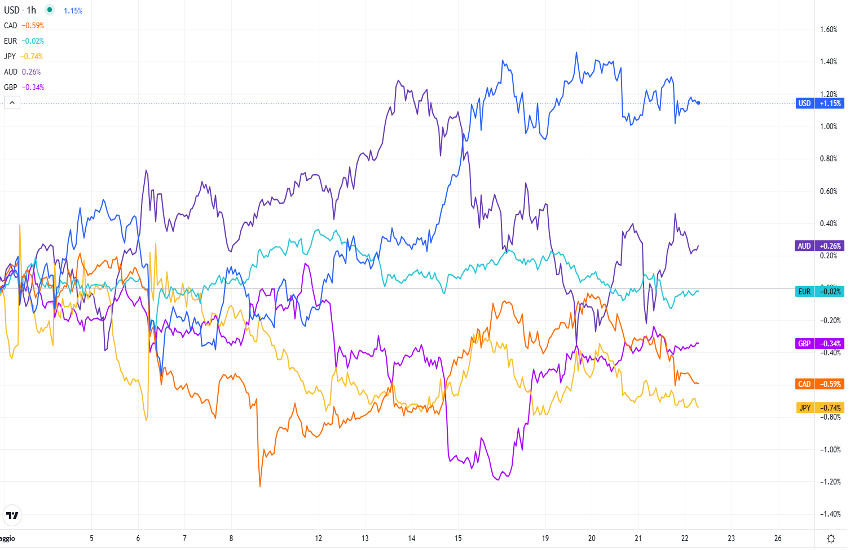

This downside inflation surprise helps explain the depreciation of the Canadian dollar during May, reflected in the rise of the USDCAD pair. The pair has moved from a low of 1.3549 at the start of the month to around 1.3787. At the same time, U.S. dollar strength has contributed to the move, with the DXY index rebounding from 97.46 to 98.98 over the same period. Overall, the Canadian dollar has been the weakest-performing major currency this month, with only the Japanese yen underperforming.

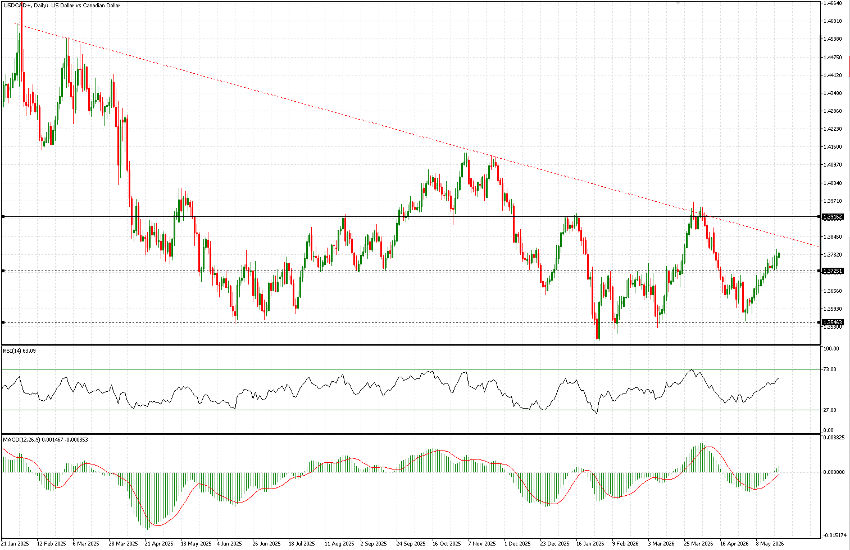

On the daily chart, USDCAD shows a strong short-term uptrend, with only two bearish sessions recorded throughout the month. The pair rebounded from the 1.3550 area, which has consistently acted as a strong support level over the past year.

A series of lower highs has been in place since January 2025, with the descending trendline currently intersecting near 1.3850, approximately 65 pips above current levels. This area is likely to be tested in the near term and represents a key resistance zone.

A confirmed breakout above 1.3850 would open the path toward the next resistance level at 1.3915. Such a move would likely coincide with the U.S. Dollar Index retesting the psychological 100 level. The base-case scenario, however, continues to maintain 1.3850 as resistance, while immediate support is located near 1.3725.