Over the weekend, markets were driven by a series of conflicting geopolitical headlines. On Saturday, reports suggested a potentially imminent attack by the US and Israel on Iran. This was followed by a sharp reversal, with reports indicating that a deal was close to being signed alongside a proposed 60-day truce. Iran denied several elements highlighted by the Trump administration, raising doubts about the substance of any agreement.

What remains clear is that diplomatic efforts are intensifying. Pakistan’s Army Chief Munir travelled to Tehran in an attempt to broker negotiations. At the same time, US Secretary of State Rubio stated that all diplomatic avenues would be explored before considering alternative options.

Despite reduced liquidity due to Memorial Day, markets reacted decisively. Oil prices dropped sharply by 6.5%. The US 10-year Treasury yield also declined, reflected in a 0.44% rise in the corresponding futures contract. This supported gains in precious metals.

Silver is up 2.88% to $77.68, while gold is appreciating by 1.05%. This confirms silver’s high-beta nature relative to gold, meaning it tends to amplify price movements in both directions.

Technical Analysis

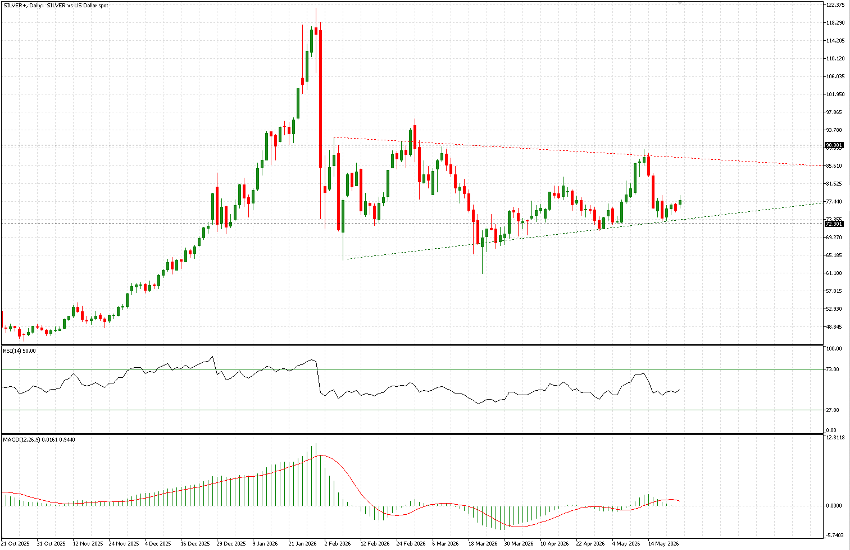

Following the sharp decline at the beginning of January, which came after an extended and aggressive rally, silver entered a consolidation phase. Price action has stabilised within a broad range between approximately 72 and 90.50.

Within this range, a compression pattern is forming, characterised by descending highs and rising lows, resembling a triangle structure. However, price continues to show weakness near the upper boundary. Each attempt to move into the 85–90 zone has been rejected, including the latest move observed a couple of weeks ago.

Price has recently retested the lower boundary, reaching a low of 73.07 last Tuesday. As long as the triangular structure remains intact, the base-case scenario points to a gradual move higher, with 87 as a potential target.

While the current upward move in silver is supported by declining yields, the broader outlook for metals remains uncertain. The relationship between real yields and inflation continues to be a key driver.

Oil prices, despite the latest pullback, have traded between 40% and 60% higher over the past three months compared to levels seen before the end of February. Despite optimism in equity markets, it remains difficult to assume that these elevated price levels will not eventually feed into broader inflation dynamics.

As a result, expectations for a sharp and sustained decline in interest rates may prove overly optimistic. While the current move higher in silver may offer tactical opportunities, the broader strategy may favour selling strength rather than buying dips in the current environment.