Tonight marks Kevin Warsh’s first press conference as the 17th Chair of the Federal Reserve, and markets are bracing for a meeting that’s as much about communication as it is about rates. Warsh was confirmed on May 13 and sworn in on May 22—just weeks after Jerome Powell’s term ended—and he inherited a fractured committee: April’s hold passed 8 to 4, with dissents pulling in opposite directions.

The rate decision itself is largely a foregone conclusion, with CME FedWatch showing roughly a 97% probability that the Fed keeps its target range unchanged at 3.50%–3.75%. What makes tonight genuinely consequential is the broader institutional overhaul Warsh appears ready to begin. He has been openly critical of the Fed’s forward-guidance model, arguing that telegraphing rate paths causes policymakers to hold onto forecasts longer than they should—a dynamic he blames for the Fed’s costly “transitory” inflation miscall in 2021–22.

His vision points toward a leaner, less verbose central bank—one that waits until it’s in the room before committing to a direction.

The most closely watched subplot tonight is whether Warsh submits his own dot to the Summary of Economic Projections. While the SEP and dot plot are still expected to be published, it would not be surprising if Warsh declined to submit his own projections—a decision that would be largely symbolic but would reinforce his view that policymakers should focus more on incoming data than on forecasts.

The rest of the committee’s dots are already shifting hawkishly. The June SEP (Summary of Economic Projections) is expected to show the median participant projecting no cuts this year, a meaningful shift from March, when at least one cut was still pencilled in. Bank of America has flagged that at least three FOMC members could project outright rate hikes in 2026—a scenario that would represent a significant repricing of risk across asset classes.

If Warsh withholds his dot and the statement drops its easing bias, markets will have a clear signal: the Powell-era playbook of telegraphed guidance is being retired, and the new Fed chair is comfortable with ambiguity as a policy tool.

Technical Analysis

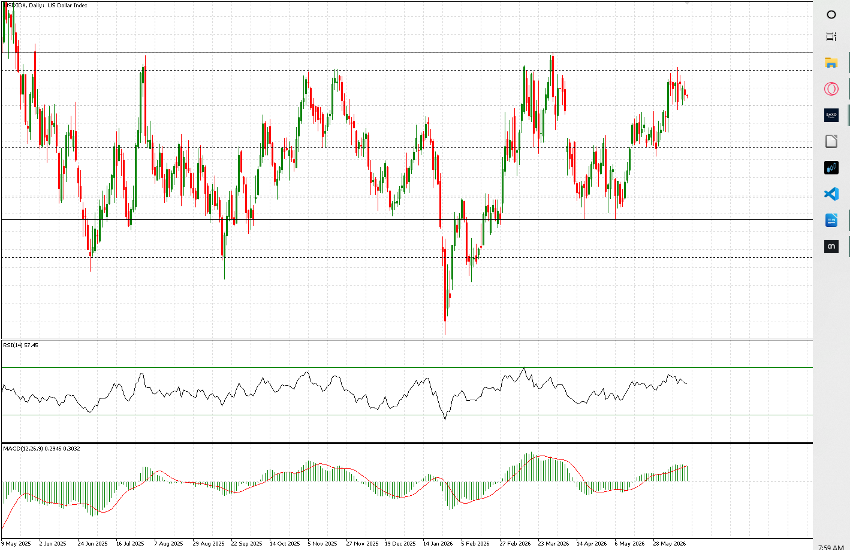

As for the U.S. dollar and the U.S. Dollar Index, the greenback has shown renewed strength since mid-April. After finding support around 97.30 and forming a relative double bottom, it gathered enough momentum to launch a fresh advance toward the current level of 99.55. As a result, it is now trading in the upper portion of the range that has contained price action over the past year, with the extreme upper boundary located around 100.30.

The 99.80 area represents another key resistance level, which was, in fact, tested last week, creating a compression zone between 99.35 and 99.80. It is worth noting that this marks the second clear period of consolidation within the broader bullish impulse. The first occurred from mid-May through early June, when the index remained trapped between 98.60 and 99.15–99.20.

These are essentially all the key technical levels that matter at this stage. Even allowing for the potential volatility following the policy decision and during the subsequent press conference, it appears highly unlikely that the U.S. Dollar Index will push significantly beyond this range.

Finally, it is worth clarifying the market’s current stance on the interest-rate path. The futures curve points to an extended period of policy stability, with only a very slight bias toward the possibility of another rate hike. From September onward, probabilities marginally favour higher rates, although the difference is minimal. The market currently assigns a 42.5% probability to a policy rate of 3.75%–4.00%, compared with 40.7% for the alternative outcome.