Attention centred on US inflation data this week, with investors looking for fresh signals on the Federal Reserve’s policy outlook and the US dollar. Kevin Warsh’s first meeting as Federal Reserve Chair was initially expected to mark the arrival of a rate cutting Trump loyalist. Instead, it delivered a hawkish surprise.

The June FOMC meeting significantly reduced forward guidance, split the dot plot 9 to 9 in favour of further rate hikes, and raised the median 2026 rate projection to 3.8% from 3.4%. Warsh also declined to submit his own dot projection.

The surprise triggered a sharp decline in EURUSD, pushing the pair below its year long 1.15 to 1.1825 trading range and to its lowest level since May 2025 at 1.1325. The hawkish shift strengthened the US dollar by reducing the euro’s relative appeal.

During his congressional testimony this week, Warsh reinforced the message by stating that “there’s still plenty of work to do,” while rejecting any suggestion that the inflation fight was complete. As a result, EURUSD remained near multi month lows around 1.14 as markets waited for signs of a policy shift that never came.

Market sentiment changed sharply following a series of weaker than expected inflation reports. Tuesday’s Consumer Price Index fell 0.4% month on month, marking the first outright decline in inflation since 2020. The reading significantly exceeded expectations on the downside and reduced the probability of a July rate hike from 42% to below 17%.

The two year US Treasury yield dropped as much as 14 basis points, recording its largest one day decline in months as traders unwound the hawkish positioning established after the June FOMC meeting.

Wednesday’s Producer Price Index reinforced the softer inflation narrative. Producer prices declined 0.3% against expectations for no monthly change, while core PPI also missed forecasts. The resulting decline in short term Treasury yields supported renewed buying interest in EURUSD as markets partially reversed expectations for further Fed tightening.

Despite the weaker inflation data, expectations for another rate hike have not disappeared.

Markets continue to price a 50% to 60% probability of a September rate increase, suggesting investors still expect the Federal Reserve to maintain a restrictive stance. With the FOMC remaining evenly divided and Warsh refusing to rule out further tightening, EURUSD’s next major move will depend on whether the recent inflation data marks the beginning of a sustained disinflation trend or proves to be only a temporary pause.

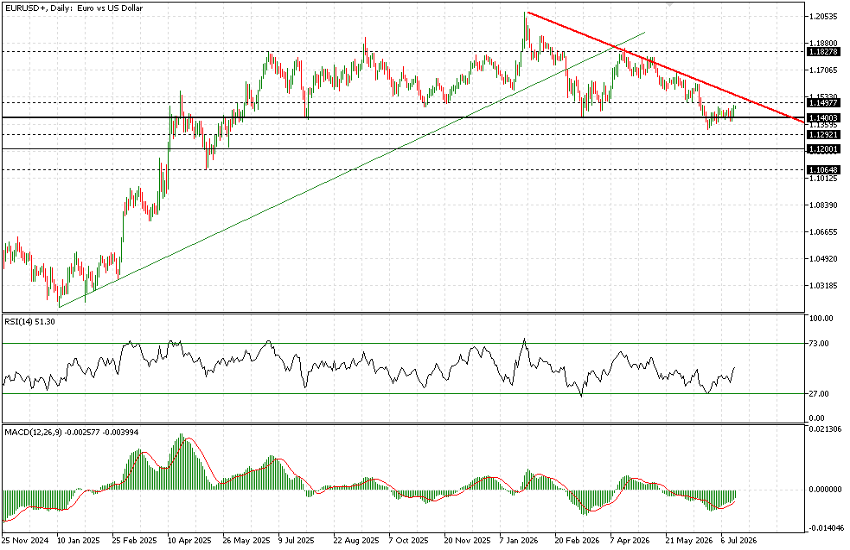

Technical Analysis

Although EURUSD traded largely within the 1.15 to 1.1825 range over the past year, there have been several notable moves beyond these boundaries. On the downside, the psychological 1.14 level has served as a key support area, acting as the final line of defence in both August 2025 and March 2026.

While EURUSD has briefly traded below 1.14 during several recent sessions, the broader support area continues to hold, with the pair currently trading at 1.1468.

Technical indicators have recovered modestly. However, 1.15 has now become a significant resistance level, reinforced by the well defined descending trendline that has guided price action throughout 2026.

In addition, the longer term uptrend that began in December 2024 appears to have been broken in March. While this does not necessarily indicate a complete trend reversal, it does suggest that EURUSD has entered a different market regime.

Overall, we remain cautious on EURUSD. If energy prices resume a sustained upward trend, we believe there is further, although likely limited, scope for additional US dollar appreciation.

Our primary downside target remains 1.1200, with intermediate support around 1.1290 and the possibility of an extension toward 1.1065.