Apple shares came under sharp pressure yesterday, closing 6.12% lower in their worst single-day performance in more than a year. The decline erased roughly $265 billion in market value, although the company remains valued at more than $4 trillion.

The sell-off followed Apple’s announcement of broad price increases across its Mac and iPad product lines, including the MacBook Neo, MacBook Air, MacBook Pro, iPad Air, and iPad Pro. The new pricing is now live across Apple’s global online store.

The primary driver behind the increases is what analysts have dubbed “RAMageddon”—a global shortage of dynamic random-access memory (DRAM) driven by the rapid expansion of AI data centres. Companies such as Nvidia have secured long-term supply agreements with memory manufacturers, diverting supply away from the consumer electronics market.

Apple is not alone. On the same day, Microsoft announced its third significant price increase for current-generation Xbox consoles, warning that storage and memory costs have already risen more than 2.5 times and could double again by late 2027.

Despite the recent share price weakness, Apple’s long-term AI strategy continues to differentiate it from many of its peers. Rather than competing directly to build the industry’s leading proprietary large language model, the company appears to be treating AI models as interchangeable services while focusing on distribution, privacy, and ecosystem integration.

Apple has reportedly agreed to pay around $1 billion annually to integrate Google’s Gemini into a revamped Siri, running through its Private Cloud Compute infrastructure. This approach enables the company to roll out AI capabilities across its installed base of more than 2.3 billion active devices.

The company has also expanded its partnership with Anthropic to integrate Claude into Xcode as a coding assistant while reportedly evaluating Anthropic’s models as part of Siri’s long-delayed overhaul. At the same time, Apple continues to invest in proprietary hardware, accelerating development of its AI-focused M7 chip generation for 2027 and an AI server chip, codenamed Baltra, in partnership with Broadcom.

Rather than competing in the AI model arms race, Apple is positioning its integrated hardware, privacy ecosystem, and global device footprint as its primary competitive advantage. While the AI infrastructure boom is contributing to higher hardware costs today, it also supports the long-term strategy underpinning Apple’s next generation of silicon and AI services.

Technical Analysis

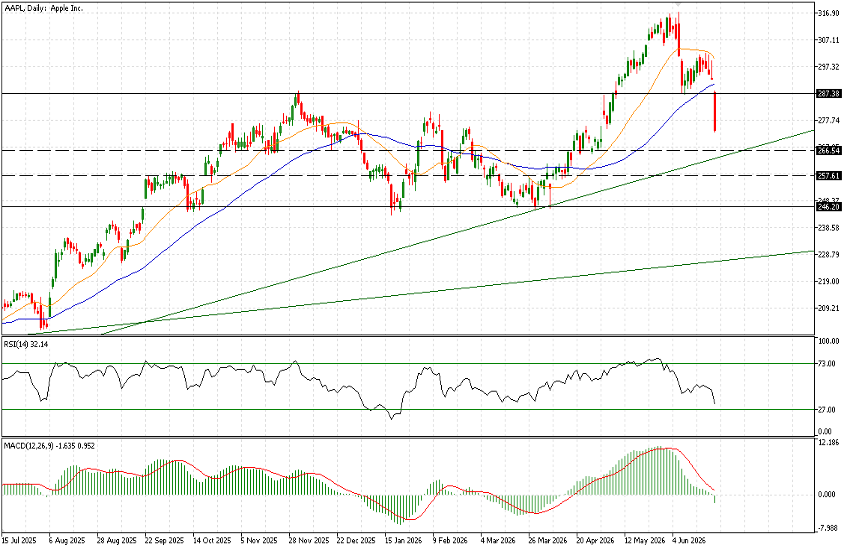

Despite yesterday’s sharp decline, which saw AAPL close at $274.03 after finishing the previous session at $292.78, the chart has not yet suffered a major technical breakdown. From a longer-term perspective, the broader trend remains bullish.

The primary ascending trendline originated in March 2025 and was reaffirmed in April this year near the $246 level.

The sell-off followed a break below the $286 support level after a gap-down opening, with selling pressure accelerating throughout the session.

While the $272 area may provide limited near-term support, $266.54 remains the key level to watch, as it coincides with the long-term ascending trendline. A decisive break below this level would represent the first meaningful technical warning signal.

Should downside momentum persist, the next support levels are located at $257 and, more importantly, $246.

Technical indicators continue to weaken. Both the RSI and MACD remain under pressure, while the widely followed 21-day and 50-day moving averages are now trading above the current price. Although these moving averages have yet to produce a bearish crossover, they continue to reflect weakening momentum.

Overall, caution remains warranted on AAPL, consistent with our recent technical view of the stock.