The Bank of Japan raised interest rates to 1%, broadly in line with expectations, bringing them to their highest level since 1995. The decision passed with a 7–1 vote, reflecting strong conviction among policymakers.

The Japanese yen remains structurally weak due to the significant interest rate differential with other major currencies. Between April 30 and May 6 alone, Japan reportedly spent nearly USD 75 billion in foreign exchange interventions to push USDJPY down from 160 to around 155.50. However, the impact of those operations has now been almost entirely absorbed by the market.

Interventions of this kind do not alter the underlying structural picture. At the same time, a rising yield curve creates considerable challenges for Japan’s banking and insurance sectors, which hold substantial exposure to the country’s public debt.

One encouraging development is that long-term government bond yields, particularly the 10-year and 30-year Japanese Government Bonds (JGBs), have stopped rising since mid-May after the 30-year yield briefly exceeded 4%. This may partly reflect moderating consumer inflation, although much of the improvement stems from the government’s fiscal support measures aimed at containing price pressures.

For 2026, the support program amounts to roughly USD 800 billion, consisting of an initial USD 770 billion package followed by an additional USD 20 billion in subsequent measures.

Meanwhile, producer price inflation has accelerated significantly, with the weak yen continuing to amplify imported inflation pressures. After an initial period of concern over the scale of government spending and its implications for the fiscal deficit, investors appear to have regained confidence and returned to long-dated fixed-income securities, pushing yields lower. The Bank of Japan’s bond purchase program, currently amounting to approximately USD 17 billion per month, has also helped support demand.

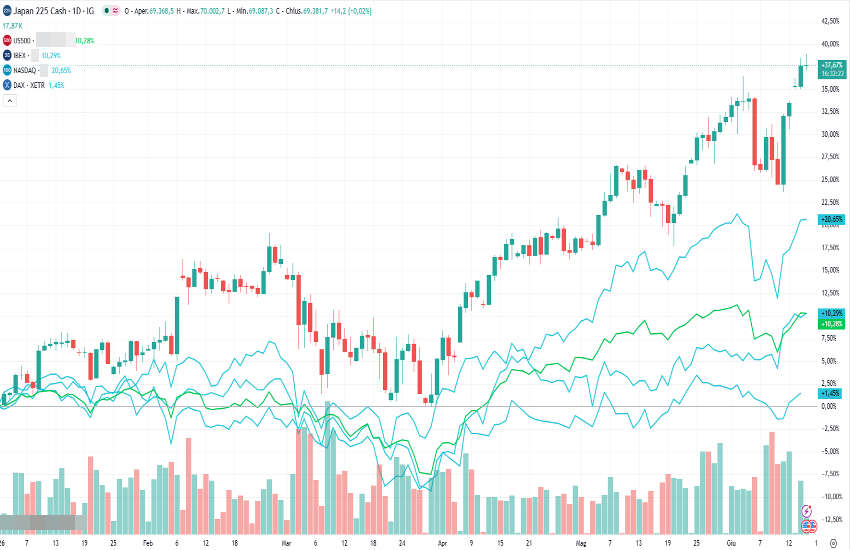

Another positive takeaway for investors is that the Nikkei has been the best-performing major equity index in 2026, gaining approximately 38% year to date. The weakness of the yen has undoubtedly been a key contributor to that performance.

For policymakers, however, equity market gains are secondary. A weak yen remains a structural challenge, even if it is one that Japan’s monetary authorities and government must continue to tolerate for the foreseeable future.

Technical Analysis

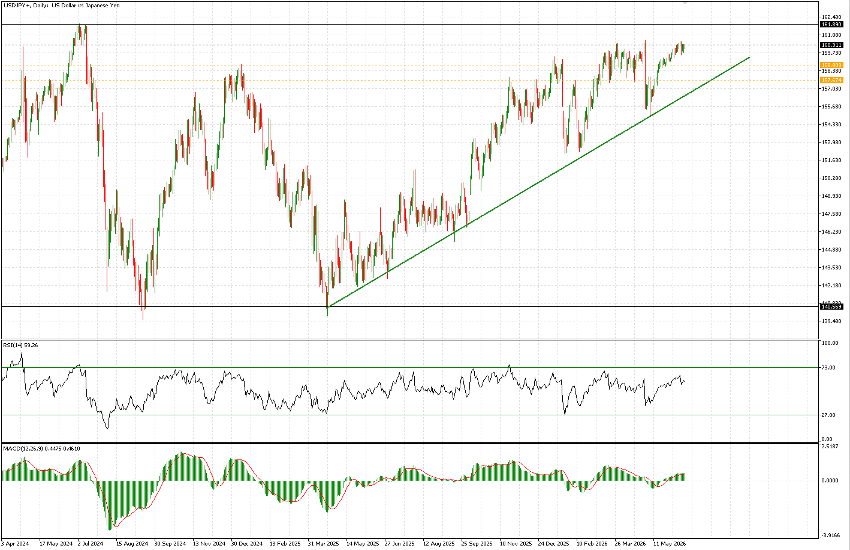

USDJPY is now in a remarkably similar position to where it traded at the end of April, just days before the intervention described above.

The broader view remains unchanged. Structurally, the yen continues to be a currency to sell, meaning USDJPY remains a long-term buy. However, once the pair moves above 160, it enters what can reasonably be considered intervention territory.

Two years ago, authorities allowed USDJPY to climb to nearly 162 before intervening. That operation triggered a decline of approximately 2,000 pips.

A similar approach may be adopted this time. Policymakers could allow USDJPY to remain largely driven by market forces and potentially rise toward the 162 area before stepping in. Delaying intervention would provide additional time to assess the impact of the latest rate hike and the broader monetary normalization process underway in Japan.

As a result, there may still be room for further upside in the pair. However, once the Bank of Japan, likely in coordination with the Federal Reserve’s trading desk, decides to intervene, it is expected to act aggressively. Historically, such operations have often taken place during New York morning trading hours.

Should intervention occur, the current price near 160.33 could reverse sharply, with support levels at 158.80 and 157.60 likely to come under pressure.

The key level to monitor is the green trendline. A retracement toward that support area could provide an attractive buying opportunity. Alternatively, a decisive break below it could signal the beginning of a medium- to long-term reversal as Japan’s monetary normalization process gains momentum.