Yesterday’s Federal Reserve meeting—potentially the last chaired by Jerome Powell—added another layer of uncertainty to markets. While Powell indicated he intended to remain on the Board of Governors in the interim, the decision to keep rates unchanged was the most divisive since October 1992, with an 8–4 split.

The dissent itself was split: three members, led by Kashkari, emphasized the need for caution, while Waller—unsurprisingly—voted for a rate cut. The outcome supported a stronger USD, further driven by speculation around potential new U.S. military action and a sharp rise in oil prices, with Brent reaching a new high since the start of the conflict.

The day prior, at its April 28 meeting, the Bank of Japan held its policy rate steady at 0.75%, maintaining borrowing costs at their highest level since 1995. The decision passed with a 6–3 vote, with dissenting members advocating for an immediate hike to 1.0%, citing rising inflation risks linked to Middle East tensions.

In its quarterly outlook, the BOJ sharply revised its core inflation forecast higher to 2.8% (from 1.9%), while lowering its FY2026 GDP growth forecast to 0.5% (from 1%). This reflects a stagflationary mix largely driven by surging energy prices. The decision has been interpreted as a “hawkish hold,” signaling growing discomfort with yen weakness.

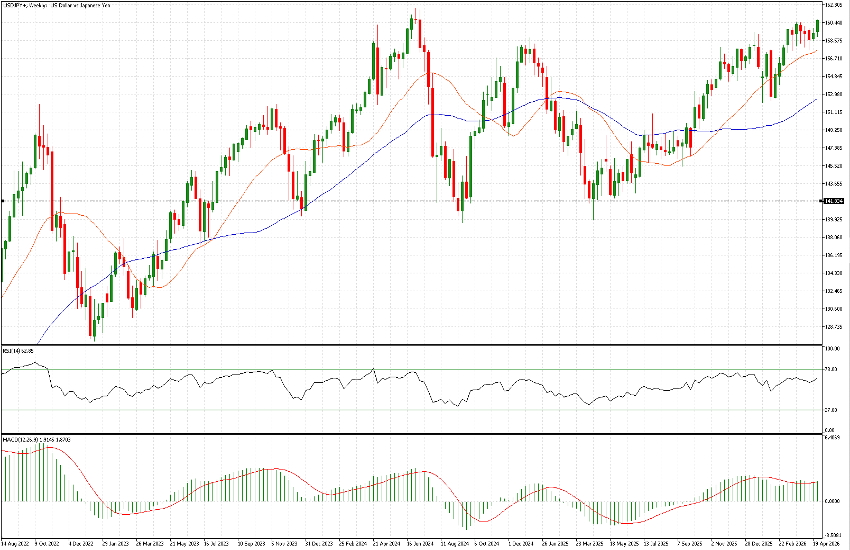

Despite this, USDJPY is trading at 160.65, near two-year highs and levels last seen in the early 1990s.

TECHNICAL ANALYSIS

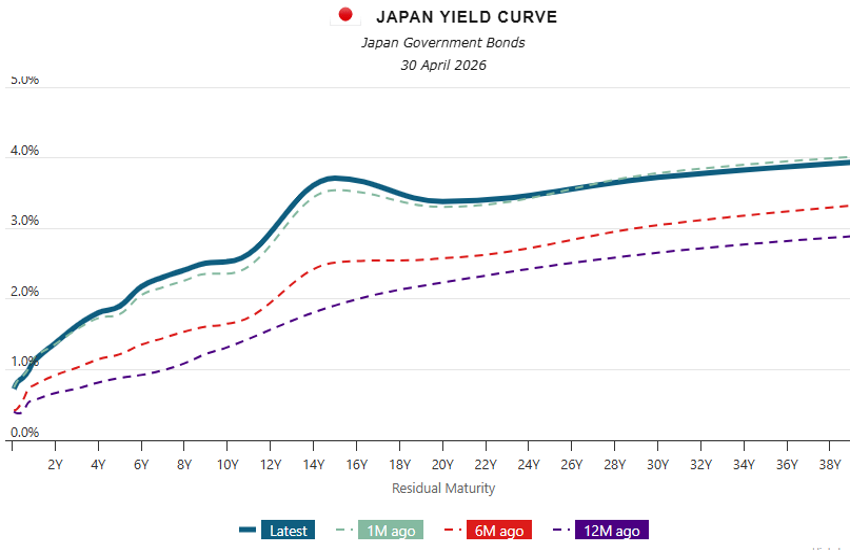

The yen remains structurally weak and widely used in carry trades due to persistent interest rate differentials. That said, some shifts are emerging, with the 10-year JGB yield at 2.53% and the 30-year approaching 4% (3.72%), although this remains an early-stage development.

The 160–161 zone has historically been a key intervention level for the BOJ, often in coordination with the New York Fed. Similar action may be expected near these levels. Notably, such interventions are typically executed during early U.S. trading hours to maximise impact.

This creates a complex environment for traders. Fundamentals continue to favour yen weakness, but proximity to intervention levels introduces the risk of sharp reversals. From current levels up to around 162—roughly 140 pips—the probability of sudden downside moves increases significantly.

One supporting factor for further upside is that previous intervention levels in 2022 and 2023 were closer to 150. This raises the possibility that authorities may tolerate further depreciation toward higher levels, potentially around 165, although this remains speculative.

From a longer-term perspective, the weekly chart suggests that optimal long entry points tend to emerge after intervention, typically within a one- to two-month window. So far, the 142 level has provided a strong entry zone and would likely attract renewed interest should the pair retrace to that area.