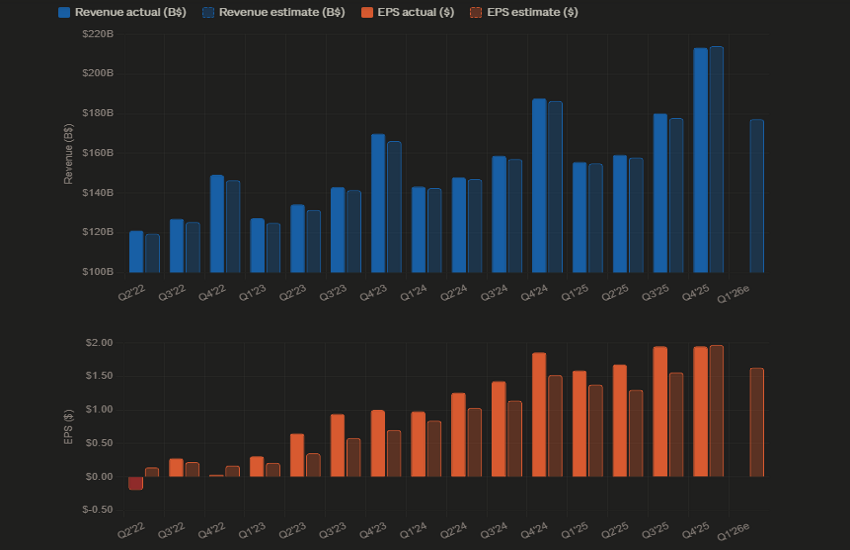

Amazon reports Q1 2026 results today after the close, with Wall Street expecting a solid but unspectacular quarter. Consensus estimates point to EPS of $1.63 (a modest 2.5% year-on-year increase) and revenue of approximately $177 billion, representing roughly 14% annual growth. Amazon has guided for operating income of $16.5–$21.5 billion, with the unusually wide range reflecting uncertainty around the pace of AI infrastructure cost absorption. CapEx has expanded significantly, from $52.7 billion in FY 2023 to nearly $200 billion projected for FY 2026, making Q2 guidance and management commentary on ROI the most closely watched elements of today’s call.

On valuation, the stock currently trades at around 29x forward P/E, with the analyst consensus price target near $295.

Focusing on AWS, Q4 2025 revenue surged 24% year-on-year to $35.6 billion, marking its fastest growth in 13 quarters. For Q1 2026, consensus expects revenue of around $36.8 billion, although margins are expected to ease slightly to 35.7%. While AWS remains more than double the size of Google Cloud and significantly larger than Azure, both competitors continue to grow rapidly and compete aggressively for AI workloads.

Advertising has quietly become a second profit engine, now an $80 billion+ annualised business growing approximately 20% year-on-year, helping offset margin pressure from AI and logistics investments.

Beyond core operations, Amazon’s most ambitious initiatives include Leo (formerly Project Kuiper), a satellite internet service designed to compete with Starlink, and its custom silicon portfolio—Graviton, Trainium, and Inferentia. There are also reports that Amazon may begin selling Trainium chips to third-party data centres, positioning itself as a potential competitor to Nvidia in merchant silicon.

At the same time, Amazon’s retail dominance is facing increasing competition. Walmart continues to strengthen its logistics offering, while platforms such as Temu and Shein compete aggressively on pricing, and Shopify-powered merchants provide alternative distribution channels.

TECHNICAL ANALYSIS

The options market is pricing in a maximum post-earnings move of 2.7%. Based on yesterday’s close at $259.70, this implies an upside level of $266.71—above previous highs—and a downside level of $252.69, slightly below the prior high reached last October.

The expected move remains relatively contained, suggesting limited overnight volatility. A sustained break above last Friday’s high at $264.16 would place the stock in new territory, where existing long positions may continue to run. However, with indicators already in overbought territory, adding new positions at current levels carries increased risk.

In the event of a post-earnings pullback, key levels to monitor are $248.70, followed by $243.40 and $232.50. The 21-day moving average stands at $236.90, while the 50-day moving average sits lower, near $220—another key support level. A move toward this level would imply a deeper retracement, which remains premature given the current strength in momentum.