Japan’s equity market opened the week amid two contrasting developments. On one side, China escalated economic pressure on Japan by blacklisting four Japanese government defense research institutes and tightening export restrictions on dozens of Japanese entities. The measures targeted several units of Mitsubishi Electric and Mitsubishi Heavy Industries, along with drone maker Terra Drone Corporation and nuclear fuel processors. Beijing said the measures were a response to Japanese Prime Minister Sanae Takaichi’s remarks that Tokyo could hypothetically intervene militarily in a crisis over Taiwan.

On the other hand, Japan’s retail sales surprised decisively to the upside, rising 5.3% year-over-year versus expectations of 3.2%. The data suggest that nominal wage growth, which initially lifted inflation expectations and supported the Bank of Japan’s normalisation process, is now translating into stronger consumer demand.

Against this backdrop, Japan’s economy expanded at an annualised 2.1% in Q1 2026, while the Bank of Japan continues to shrink its balance sheet and the country’s monetary base keeps contracting. Despite these conditions, the Nikkei remains the best-performing major equity index globally and across Asia. Its annual gain of more than 35% is well ahead of U.S. and European indices, as well as regional peers such as Australia and China.

The continued depreciation of the Japanese yen has also supported the Nikkei’s revaluation. As anticipated, USDJPY continues to trade around 161.78 without triggering official intervention, allowing the pair to move toward the 162.00 area. Even after adjusting for the USDJPY closing level of 156.71 on 31 December, the Japanese index would be only around 3% lower, equivalent to approximately 67,200 points.

This morning, however, the Nikkei is among the weakest performers in Asia, down 0.80% at the time of writing, with only the more volatile Kospi posting a steeper decline.

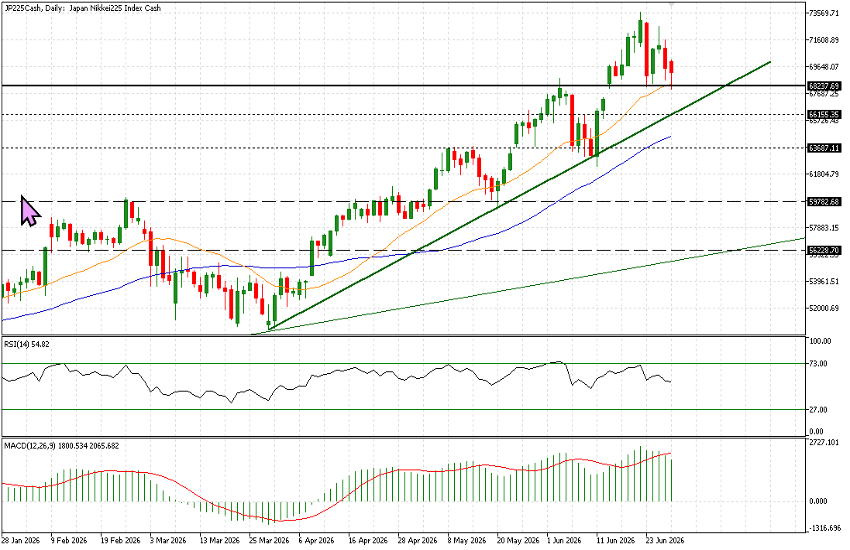

Technical Analysis

Last Friday, the Nikkei fell 4.15%, closing the cash session at 69,360. The index tested the key near-term support around 68,200 before rebounding overnight from a low of 68,017 to the current 69,250 area. The 21-day moving average also sits nearby, around 69,386.

The broader chart remains clearly bullish. The primary trendline originating on 30 March currently stands around 66,200, approximately 4.4% below current levels. The 50-day moving average continues to slope upward and remains below the 21-day moving average, currently around 64,500.

The RSI and MACD remain less stretched than price action and continue to show no signs of bearish divergence.

For now, pullbacks should continue to be viewed as potential accumulation opportunities. Aside from the steeper trend that began this spring, the Nikkei’s broader bullish structure remains intact down to around the 56,000 level.

The first key support remains 68,200, followed by 66,150 and 63,675. Only a decisive break below all three levels would shift attention toward the 59,800 area, although it is too early to consider that scenario the base case.

On the upside, the levels to monitor are 70,750, 72,000, and the all-time high at 73,630.

If broader market conditions and risk sentiment remain supportive, the Nikkei continues to offer an attractive opportunity. Pullbacks may still provide favourable entry points for investors seeking exposure to Japan’s ongoing equity market strength.