Understanding commissions—where applicable to certain instruments in your trading account—is generally straightforward: you are charged a fixed amount per transaction, or occasionally a fixed percentage, and the calculation is simple.

Where most traders struggle, however, is in understanding swap costs: what they are, how they are generated, and how to calculate them. In this post, we break them down clearly. Spreads, on the other hand, are an implicit and unavoidable market cost, yet still worth quantifying and briefly explaining.

SWAPS

Leverage often sounds almost magical in retail trading: 10x, 30x, 1000x. Behind it lies something simple but essential: leveraged capital is borrowed money, and borrowed money carries a cost.

It works much like taking out a mortgage or personal loan—only faster, more convenient, and with far less bureaucracy. If you buy $30,000 worth of EURUSD with 30:1 leverage and commit only $1,000 of your own capital, the remaining $29,000 is effectively lent to you by the broker. Naturally, interest is charged on that financing.

What Determines Swap Rates

Because swaps reflect the cost of borrowed capital, the interest rate associated with the currency underlying the instrument is the primary driver. Holding overnight exposure in a currency like JPY (with an official rate near 0.50%) is generally less costly than holding USD-denominated instruments (where the reference rate is around 3.75–4.00%).

“Overnight” is the key: swaps apply only to positions held beyond a single trading session.

To the benchmark rate, the broker applies a standard financing spread or markup—similar to how banks add a premium when they lend. This is a normal part of the cost structure.

Long vs. Short

Swap charges differ depending on whether you are long (buying) or short (selling an asset you do not own).

When you go long, the broker lends you capital, so you pay interest. When you go short, you are—conceptually—lending the asset to the broker, and in theory you should receive interest. For higher-yielding currencies (TRY, MXN), positive swaps are possible.

However, in today’s low-rate environment, once the broker markup is applied, it is unusual not to incur an overnight cost, regardless of direction.

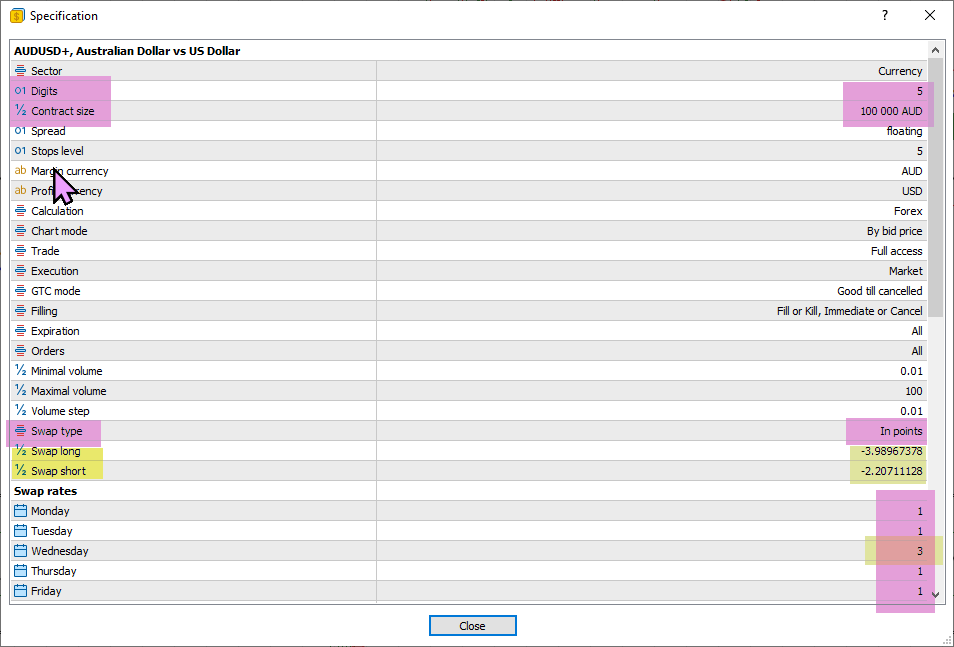

Swap Types and Triple Swaps

In “Specification,” you will typically find two swap-calculation methods: IN POINTS or IN PERCENTAGE. You will also see that swaps are tripled on one day per week—marked as “3.” For FX this is usually Wednesday; for indices and equities, typically Friday. This reflects settlement conventions and the fact that no financing is charged on Saturdays and Sundays.

Swap Calculation in Percentage

Interest rates and swaps expressed as percentages are always annual. By convention, traders divide by 360 to obtain the daily charge.

Example: if you buy an index with a 10% long swap on Monday and close it Friday morning (four overnights):

Position value × 0.10 (10%) / 360 × 4

A second example: you buy 1 lot of Apple on Thursday and close the position Tuesday. Long swap = –3% (triple swap on Friday). Contract size = 1; price = $279.

Position value = $279. Swap cost:

$279 × 0.03 / 360 × 5 days = $0.11625

Swap Calculation in Points

This method is slightly more complex because it requires factoring in the instrument’s DIGITS (visible in “Specification”). The advantage is that this rate is applied daily, not annually.

Example: you sell 1 lot of US100 on Friday at 25,405. Swap short = –14.33; contract size = 1; digits = 2; currency USD. You close Monday. With 2 digits, –14.33 means a daily charge of 0.1433 USD

(With1 digit, it would have been1.433 USD; with 3 digits, 0.01433 USD, etc.)

Friday incurs triple swap:

1 × 0.1433 × 3 = $0.4299

Position value = $25,405

Spreads

The spread is not technically a “fee” but it is unavoidable. The difference between Bid and Ask reflects natural market dynamics—demand and supply. Still, understanding its monetary impact is useful.

Example: EURUSD quoted at 1.16272 / 1.16280 → spread = 0.8 pips.

Mid-price = 1.16276.

Difference from execution = 0.00004.

Buying 1 lot (100,000 units):

100,000 × 0.00004 = 4 USD

(Profit/loss in FX is always quoted in the second currency of the pair.)

Spreads vary throughout the day:

• tighter during main cash sessions (e.g., U.S. indices from 14:30 to 21:00 GMT)

• wider overnight or during low liquidity

Conclusion

We hope this overview helps you better understand and calculate your trading costs—especially when holding positions for extended periods, where swap charges can materially impact performance.