Cisco is the world’s dominant provider of enterprise networking infrastructure, including routers, switches, and the foundational hardware that moves data across corporate and cloud networks. Its AI angle is less about building large language models and more about being the indispensable plumbing underneath them. AI workloads require massive, low-latency data movement between GPUs and servers, and Cisco is positioned as a critical enabler of that infrastructure. Hyperscalers are spending hundreds of billions building out data centres, and Cisco is among the primary beneficiaries supplying the network fabric that connects everything together.

Cisco’s stock significantly lagged pure-play AI names as investors struggled to classify it as an AI winner. It lacks the narrative clarity of NVIDIA while also carrying the legacy burden of a mature networking business.

The company also suffered from a prolonged demand hangover. Enterprise customers had overordered networking equipment during the post-COVID supply chain disruption, and the resulting destocking led to three consecutive quarters of declining revenue throughout 2024. Cisco carried out two major rounds of layoffs in 2024, eliminating more than 9,800 roles—nearly 12% of its workforce—which weakened market confidence even as management framed the move as a strategic pivot toward AI, cloud, and cybersecurity.

In addition, restructuring efforts aimed at reallocating resources toward AI created operational pressure, alongside compressed free cash flow and margin constraints.

The latest results, however, marked a clear inflection point. Cisco reported record quarterly revenue of 15.8 billion dollars in Q3 FY2026, representing strong double-digit year-over-year growth and exceeding the upper end of its guidance. EPS came in at 1.06 dollars, beating consensus expectations of 1.00 dollar.

Security revenue surged 54% year-over-year, while networking revenue grew 8%, signalling that the destocking cycle has ended. Management cited broad-based demand driven by AI infrastructure buildouts as the key tailwind.

Alongside the results, Cisco announced an additional 4,000 job cuts—roughly 5% of the remaining workforce—aimed at reallocating capital toward silicon, optics, and AI tooling.

For full-year FY2026, guidance was raised to 62.8–63.0 billion dollars in revenue, with EPS projected at 4.27–4.29 dollars. The CFO also pointed to a potential 6 billion dollar AI-related revenue opportunity by FY2027.

Technical Analysis

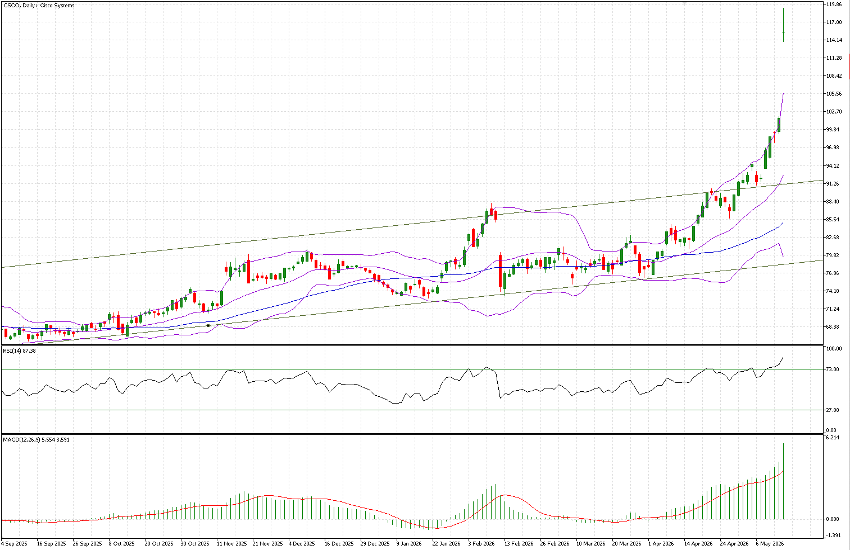

Cisco posted its strongest single-day performance since 2011, surging as much as 17.4% in extended trading before closing at 115.53 dollars, up 13.41%.

From a chart perspective, the stock printed a spinning top at the end of the rally and left an open gap of more than 12 dollars, approximately 12.5%. Gaps tend to be filled over time, making this a key technical feature to monitor.

CSCO, Daily, Sep 2025 to present

Indicators are highly overextended. The distance from the 21-day and 50-day moving averages is significant, and the upper Bollinger Band was decisively breached. The trading channel that had contained price action since the 2024 lows was also broken to the upside at the end of April.

This is a classic setup where patience is warranted. Chasing price at current levels carries elevated risk, although waiting may mean missing further upside if momentum persists.

From a trading perspective, two levels stand out. The recent high at 119.24 dollars and the gap level at 101.89 dollars provide key reference points for short-term positioning. The wide range reflects the increased volatility typical of AI-driven equities.